Here are some notable charts to monitor in commodities markets over the coming days.

Shipping

Commodity watchers keen on taking the pulse of the global economy should note that container ships — the lifeblood of trade — are traveling at the slowest speeds since Bloomberg began tracking the data in October 2020. That reflects uncertainty over the pace of China’s growth this year while the nation recovers from Covid-19 and influenza outbreaks. Unlike lagging economic indicators — Chinese import and export data for January and February won’t be released until March — shipping companies are already pronouncing a verdict on commodity demand. With no incentive to raise speeds or add more vessels to service routes, these ships are waiting for lackluster exports of steel in Asia to pick up, as well as imports of raw materials and agricultural products from around the world.

Diesel

International Energy Week kicks off in London on Tuesday, bringing together senior industry leaders, investors and government figures to discuss energy security and finance, climate change, demand from China and the fallout from Russia’s invasion of Ukraine, including the rerouting of decades-old flows across crude and refined products. In Europe, diesel is still flowing this month even after the start of sanctions on purchases from its former top supplier, mostly due to shipments from the Middle East and Asia. Total imports are set to slightly beat January’s level.

Agriculture

Keep an eye on the weather in Argentina, the world’s biggest supplier of soy meal and soy oil. With more dry conditions forecast, the dire situation for the nation’s key soybean crop could get worse. Last week, the Buenos Aires Grain Exchange slashed its production estimate to the lowest in 14 years and warned that further cuts are possible. A smaller harvest is bad news for the government, which depends on farming to drive the economy and soy exports to prop up central bank dollar reserves. The reduced harvest will also fuel global soy prices.

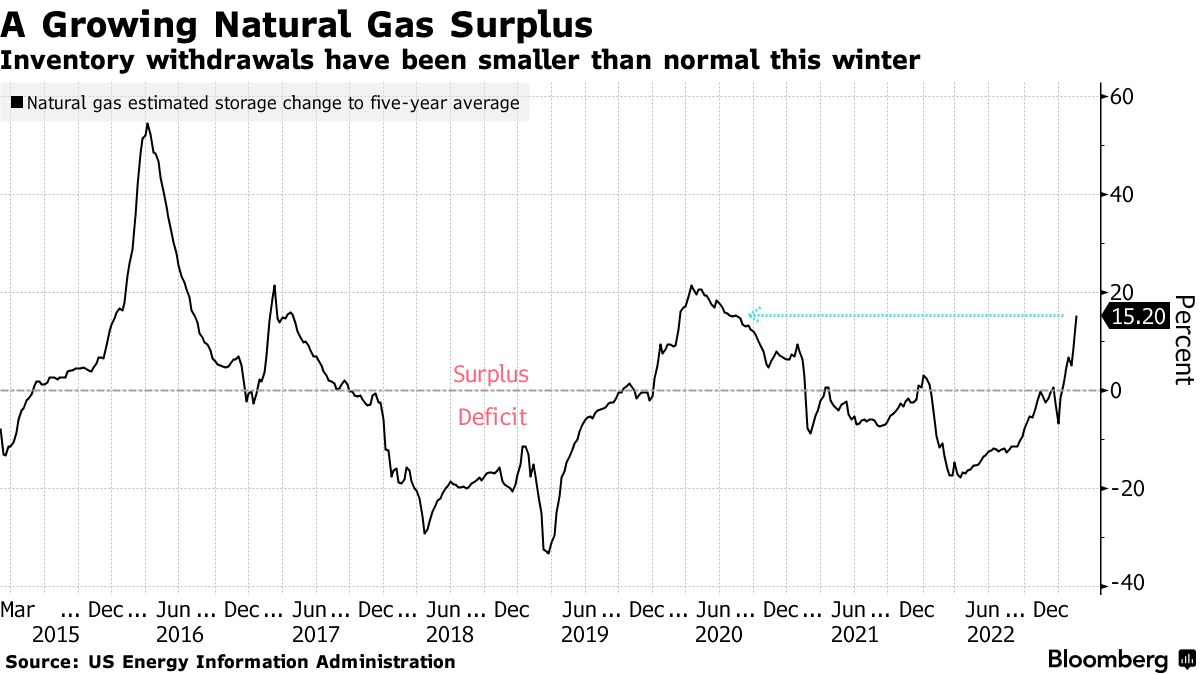

Natural Gas

The US finds itself flush with natural gas. Stockpiles of the heating and power-plant fuel versus the five-year average are at the highest level since August 2020, when consumption was blunted by pandemic-related lockdowns. A mild winter and the seasonal shift to warmer temperatures will likely see inventories climb even higher, possibly approaching levels not seen since 2016 and 2017. Futures prices have rallied in recent days after plunging below $2 per million British thermal units last week, as producers signal slower production growth.

Power

Power generators supplying PJM Interconnection LLC, which operates the largest US grid serving more than 65 million Americans from Washington, DC to Illinois, will find out how much revenue they will reap through a capacity auction for the year starting June 2024 when results are posted Monday afternoon. Prices plunged in the previous two auctions because of persistent excess supplies, and while notoriously difficult to predict, many expect the so-called capacity clearing price to sink further. That may do little to stem the glut because many generators made record profits last year amid a rally in electricity prices, creating a lifeline. However, capacity prices are at risk of jumping if a number of old plants shut down or there are delays for completing new plants.

Written by: Sophie Caronello — With assistance from Jonathan Gilbert, Naureen S Malik, Ann Koh, Amanda Jordan, Gerson Freitas Jr, Kevin Varley, and Prejula Prem @Bloomberg

The post “Five Key Charts to Watch in Global Commodity Markets This Week” first appeared on Bloomberg