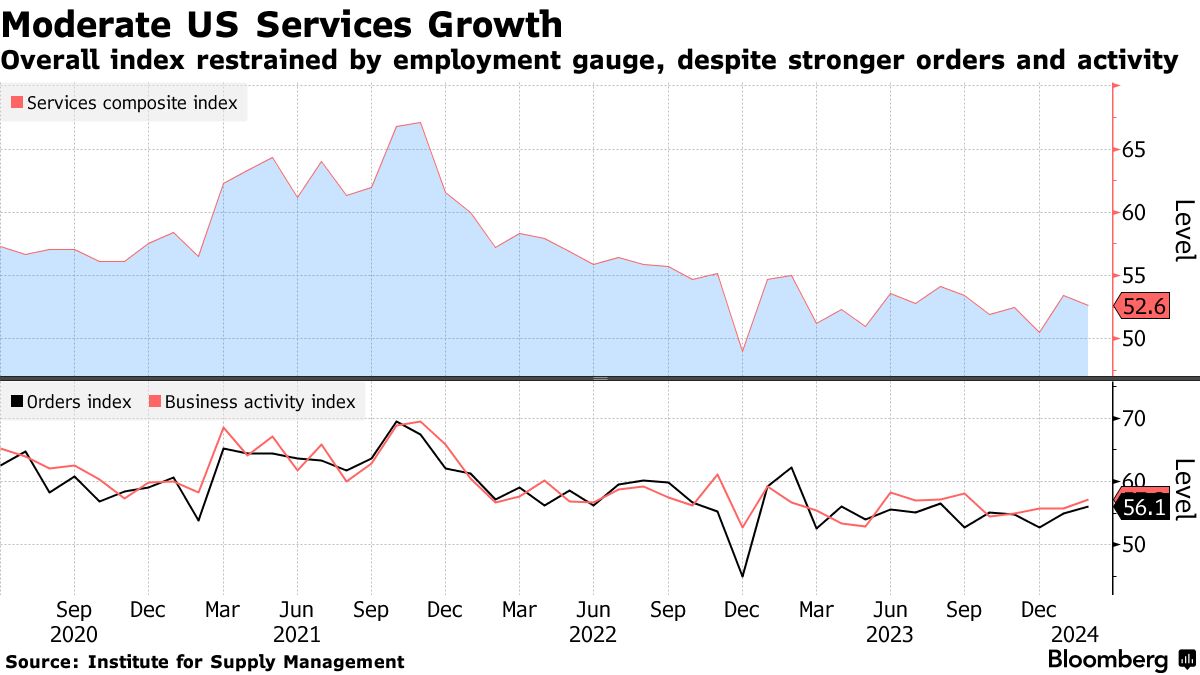

- ISM services PMI decreased 0.8 point in February to 52.6

- Employment measure declined; gauge of prices paid dropped

Growth in the US service sector cooled in February, partly due to a decline in employment even as orders and business activity quickened.

The Institute for Supply Management’s composite gauge of services slipped 0.8 point to 52.6 last month. The index has held above the 50 level that indicates expansion for more than a year. The median estimate in a Bloomberg survey of economists called for 53.

The ISM measure of services employment fell back into contraction territory last month, to 48. The gauge of supplier deliveries dropped 3.5 points to 48.9, the lowest since October and indicating improved delivery times.

At the same time, other demand measures strengthened. The gauge of new orders placed with service providers — a proxy of future demand — increased to 56.1, the highest since August.

“The majority of respondents are mostly positive about business conditions,” Anthony Nieves, chair of the ISM Services Business Survey Committee, said in a statement. “Respondents remain concerned about inflation, employment and ongoing geopolitical conflicts.”

Based on comments from survey respondents, the drop in the employment index is the result of a companies shedding workers or being cautious about hiring and also difficulty recruiting and hiring qualified workers.

Fourteen service industries reported growth last month, led by construction, retail trade and public administration.

The group’s business activity index, which parallels ISM’s factory output gauge, climbed to a five-month high of 57.2. While the measure of manufacturing production shrank last month, purchasing managers remained optimistic about the direction of the sector.

Meanwhile, costs of materials are rising at a slower pace. The index of prices paid by service providers fell 5.4 points, the most since July 2022, to 58.6 in February.

Select ISM Industry Comments

“Business remains strong across the U.S. industrial construction sector. Construction materials levels have returned to pre-coronavirus pandemic levels, and the outlook for 2024 is strong.” – Construction

“Continued inflationary pressures and labor price increases are challenging, but we continue to push forward.” – Health Care & Social Assistance

“Employers remain cautious about hiring direct employees and are considering utilizing contract labor to cover project and interim work demands as concerns about the economy continue to be front of mind.” – Management of Companies

“Commodity prices have dropped in the last quarter, although they have been range-bound over the last year. Production continues steady increase.” – Mining

“Economy seems unsettled. Inflationary fears persist, yet some things are settling down. High demand for services, although inquiries from contractors for opportunities seem to be only inching upward. Layoffs in many large industries, but many businesses are desperate for workers. Lots of contradictions.” – Public Administration

“Business is good. Inflation is under control and trending downward. Pricing of commodities is going up at a slower pace.” – Retail Trade

“Labor continues to be in highest demand. Finding qualified and available crews and administrative staff (is still) difficult.” – Utilities

“Moderate increases in business activity so far. Improved supplier fill rates and steady pricing have resulted in increased levels of restocking as businesses prepare for spring and summer selling seasons.” – Wholesale Trade

The improvement in delivery times and greater progress on order backlogs suggest supply and demand is in better balance. Moreover, a measure of inventories contracted the most since the end of 2022.

A gauge of sentiment about inventory levels also fell, indicating respondents see their stockpiles becoming more in line with demand.

Written by: Mark Niquette — With assistance from Kristy Scheuble @Bloomberg

The post “US Services Growth Cools While Orders, Business Activity Pick Up” first appeared on Bloomberg