- Alliance to unwind production cutbacks from the fourth quarter

- Demand concerns, signs of ample supplies add to declines

Oil fell to the lowest in about four months after OPEC+’s plan to loosen its production curbs this year deepened the market’s bearish sentiment.

The output cuts are scheduled to start unwinding as early as October, adding barrels to a market beset by persistent concerns about demand and robust supplies from outside the group. The perception that geopolitical risks to crude supplies are ebbing has also added to the declines.

West Texas Intermediate fell 1.3% to settle above $73 a barrel, with algorithmic commodity-trading advisers contributing to the dip. Still, prices regained some ground after falling as much as 2.3% earlier in the session.

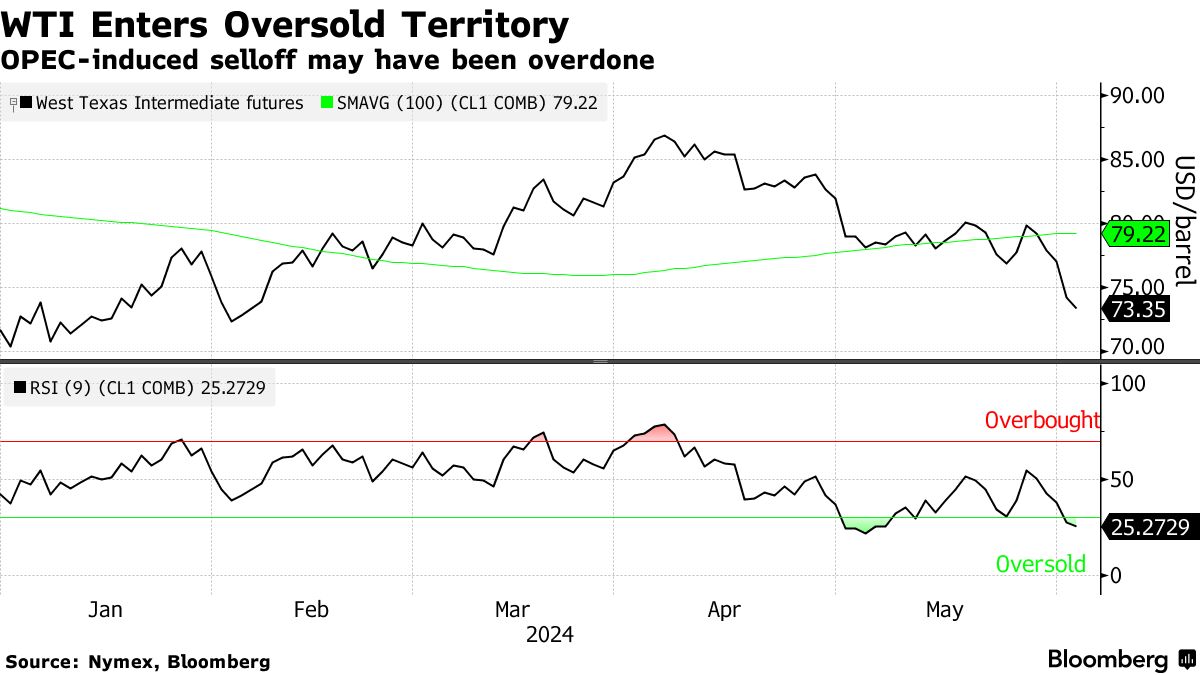

“We hit oversold levels in WTI this morning with RSI falling below 30, so we were set up for some relief,” said Rebecca Babin, senior energy trader at CIBC Private Wealth Group. “Secondly, crack spreads and time spreads are stronger today, which is a positive for physical market indicators and usually leads crude out of a selloff.”

International benchmark Brent crude fell below $80 per barrel for the first time in four months on Monday, and Tuesday marks the first time Brent breached the threshold on its 14-day relative strength index since May 2023.

Some market watchers had expected OPEC+ to extend cuts through to the end of the year, and reaction to Sunday’s deal was mixed, including doubts about whether the group will be able to ramp up production as rival supply surges. Key alliance members have pumped above their assigned quotas recently as well.

Even so, the intention to produce more will have a psychological effect on markets, analysts at Engie SA’s EnergyScan wrote in a note. The United Arab Emirates was given a 300,000 barrel-a-day boost to its production target for next year.

“The consequence is lower oil prices in a context of oversupply,” they said.

Written by: Jordan Fitzgerald and Julia Fanzeres @Bloomberg

The post “Oil Slides to Four-Month Lows as OPEC+ Deepens Bearish Sentiment” first appeared on Bloomberg