- Swaps imply at least five quarter-point cuts by Fed this year

- Dovish repricing follows weaker-than-expected US jobs data

Global bonds rallied as traders bet the Federal Reserve and fellow central banks will turn more aggressive in cutting interest rates amid mounting signs that economic growth is faltering more quickly than expected just weeks ago.

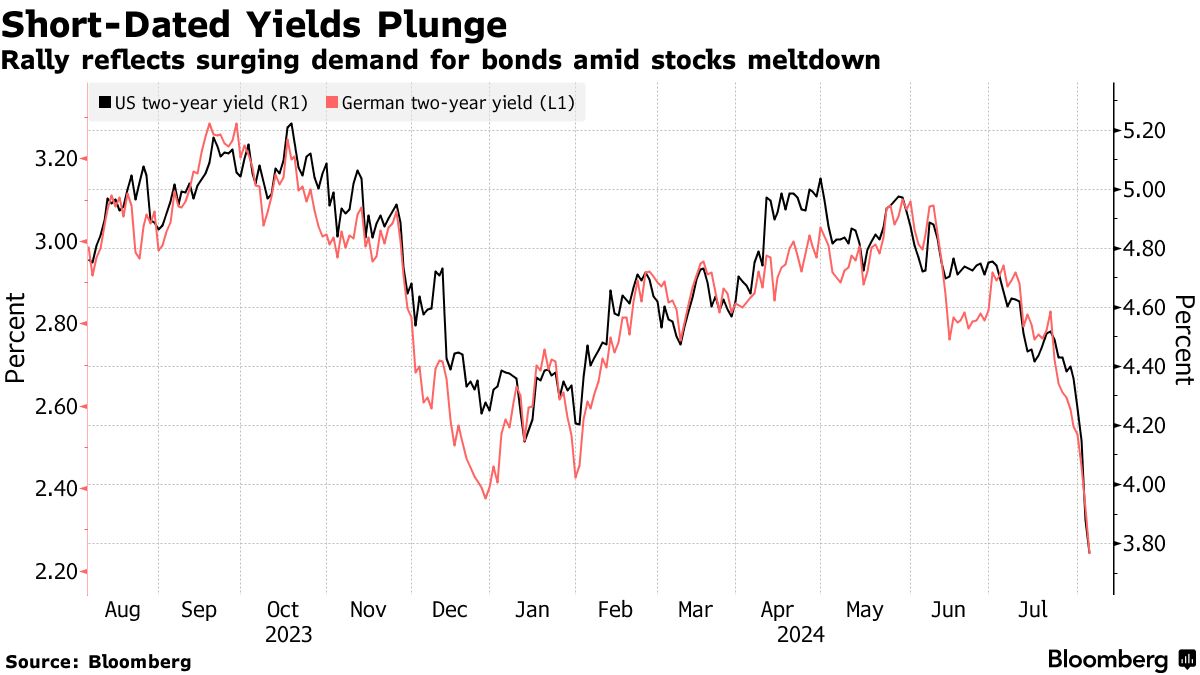

Short-dated debt — the most sensitive to changes in monetary policy — led the move, with the US two-year Treasury yield falling as much as 23 basis points Monday to 3.65%, the lowest in over a year. The two-year yield dipped below the 10-year for the first time since July 2022, when Fed interest-rate increases drove short-term yields higher. In Europe, equivalent German yields tumbled by a similar amount to 2.15%.

The global repricing was so sharp that at one point interest-rate swaps implied a 60% chance of an emergency rate cut by the Fed in the coming week — well before its next scheduled meeting on Sept. 18. While those odds subsequently ebbed to about 32%, the wager is a testament to investor anxiety.

Driving the shift in sentiment is mounting evidence that the world’s largest economy is slowing, suggesting the Fed may have fallen behind the curve in holding rates steady last week. A global rout in equities and sharp unwind of a once-popular and crowded strategy in the currency market, known as the carry trade also sent investors into the relative safety of sovereign debt.

US July jobs data and a manufacturing sector gauge released last week were much weaker than expected, leading traders to bet on at least five quarter-point rate cuts from the Fed by year-end, compared with just two expected a week ago. The wagers were pared slightly on Monday after a gauge of services activity was stronger than anticipated.

“The global easing cycle has well and truly begun,” said Michael Ford, co-deputy head of the multi-asset strategy team at Insight Investment. The “widespread nature” of cuts reflects the fact that policymakers are becoming as concerned about growth as inflation, he added.

Economists at Citigroup Inc. and JPMorgan Chase & Co. last week predicted that the Fed will lower its benchmark by a half-point at both its September and November meetings.

Treasury yields across maturities remain at least five basis points lower on the day after paring declines. The brief return of a normal, upwardly sloping yield curve was a key milestone for the market, as some investors ascribe to the end of a period of inversion a signal that the economy is on the doorstep of a recession.

Friday’s increase in the unemployment rate caused its three-month moving average to exceed the 12-month low by half a percentage point. According to the Sahm rule — devised by former Fed economist Claudia Sahm — that means a recession is underway.

Traders also amped up wagers on the extent of easing from the European Central Bank, which cut rates in June for the first time in years but held steady last month. Swaps imply about 80 basis points of additional cuts through 2024, with a just under 20% chance of a half-point reduction in September.

In Japan — where the central bank only just started hiking — the 10-year benchmark yield tumbled around 20 basis points as the nation’s stocks toppled into a bear market. Similar-maturity New Zealand yields slipped 10 basis points. Australia’s cash bond markets were shut for a holiday, but three-year futures surged to the highest since June 2023.

Some investors say the moves are overdone. Guillaume Rigeade, co-head of fixed income at Carmignac, doubts the Fed will need to deliver an emergency cut as soon as this month. Fed Chair Jerome Powell last week said a September rate cut was on the table.

“For sure, the economy is slowing in the US,” said Rigeade. But while the Fed may well cut next month, “we are not believing that the market should price as much as it is pricing now.”

UBS Group AG’s head of European rates strategy Reinout De Bock takes a similar view and is taking profits on positions in US and European short-dated positions. He says the market is “now running ahead of data,” adding that sharp risk-off moves aren’t unusual at this time of year, when liquidity is lower.

The massive rally has led a Bloomberg index of global sovereign debt to erase most of its 2024 losses, a remarkable turnaround for an asset class that has failed to deliver the lofty returns widely expected at the end of last year. The gauge is now down just 0.2% year-to-date, having lost more than 5% as recently as early July.

“There was a lot of focus on ‘normalization’ cuts, whereas if we have reactionary cuts, we know that the Fed has a lot of buffer so you need to incorporate the probability of very large cuts,” Christian Mueller-Glissman, head of asset allocation research at Goldman Sachs Asset Management, said in an interview with Bloomberg TV.

Written by: Alice Gledhill — With assistance from David Finnerty, Marcus Wong, Tania Chen, Alice Atkins, James Hirai, Liz Capo McCormick, and Michael Mackenzie @Bloomberg

The post “Global Bond Rally Accelerates as Market Bets on Big Rate Cuts” first appeared on Bloomberg