- Dovish Fed helps markets bounce back from early-August rout

- Data on jobs, manufacturing will test faith of economic bulls

It began badly. But four weeks on from the worst volatility blowup since the pandemic, August will go down as another grand gesture of confidence by Wall Street in its ability to suss out the future.

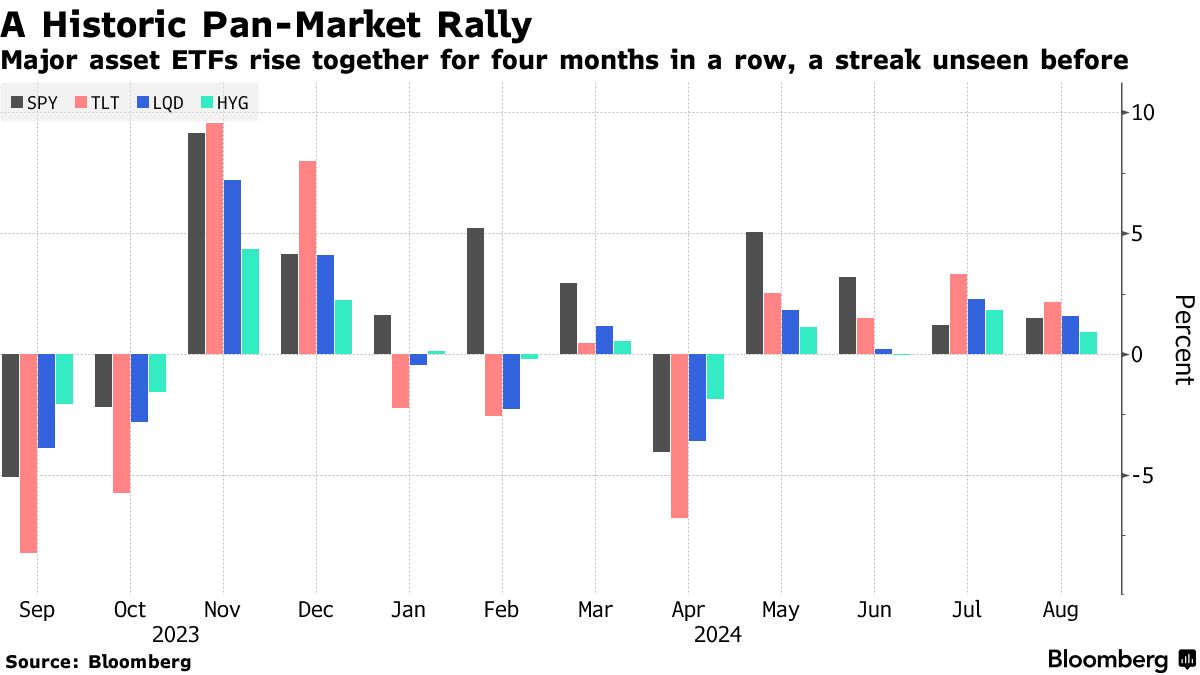

Levels of conviction are soaring across assets. In one example, exchange-traded funds tracking government debt, corporate credit and equities have now risen in unison for four straight months. It’s the longest stretch of correlated gains since at least 2007. Up 25% in the past 12 months, the S&P 500 has never climbed this much in the run-up to the first interest-rate cut of an easing cycle, seven decades of data compiled by Ned Davis Research and Bloomberg show.

Traders are leaning into bets with zeal even as serious questions linger about the economy and inflation — and how central bankers will respond. Before the Federal Reserve has even begun to act, bond markets have priced in a slew of rate cuts, measures of default risk are falling and surging equities reflect sure-thing bets the economy will boom.

Gains of 2.3% for the S&P 500 in August, 1.8% for an ETF tracking long-dated Treasuries and 1.5% for investment-grade bonds all amount to a big show of force by cross-asset bulls, who are convinced Fed Chair Jerome Powell will cut rates into a healthy economy. All told, the wagers are at the mercy of how economic data — capricious of late — plays out on the cusp of the central bank’s meeting on Sept. 18.

“Everything has to go right,” said Lindsay Rosner, head of multi-sector investing at Goldman Sachs Asset Management. “We need to continue to have trend or above trend economic growth. We need to have a labor market that’s not too hot, not too cold. And that then would allow for the consumer to continue to consume. Those things all have to be in a perfect balance.”

While markets have righted themselves, the travails of early August demonstrate the delicacy of the present consensus, with a single government report — US hiring data for July — fueling convulsions that briefly sent Wall Street’s fear gauge, the VIX, above 65. August’s employment update is just seven days away — with economist forecasts compiled by Bloomberg putting payroll additions anywhere from 100,000 to 208,000.

Data on US manufacturing, durable-goods orders and initial jobless claims are also due next week, each with the potential to influence sentiment at a time when growth has become a singular obsession of markets. At Jackson Hole, Wyoming, last week, Powell said “the direction of travel is clear” on future policy, but that “the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks.”

Fed dovishness was instrumental in pulling Wall Street’s investment complex through its summer tantrum, with the flash crash in early August quickly consigned to history. All four major asset ETFs (tickers: SPY, TLT, LQD, HYG) rose at least 1% for the month while more than $1 trillion was added to American equities alone.

Traders are pouncing on everything from small-cap stocks to speculative debt convinced that the world’s largest economy will avoid a consumer-led downturn despite a weakening labor market. Funds focused on US stocks added $5.8 billion for a ninth straight week of inflows and those specialized in high yield attracted $1.7 billion, EPFR Global data compiled by Bank of America Corp. show.

For now at least, nothing in economic data or corporate earnings is screaming danger. Yet if there is a lesson in August’s rout, it’s that consensus bets — going long artificial intelligence, exploiting the weakening yen — can backfire suddenly.

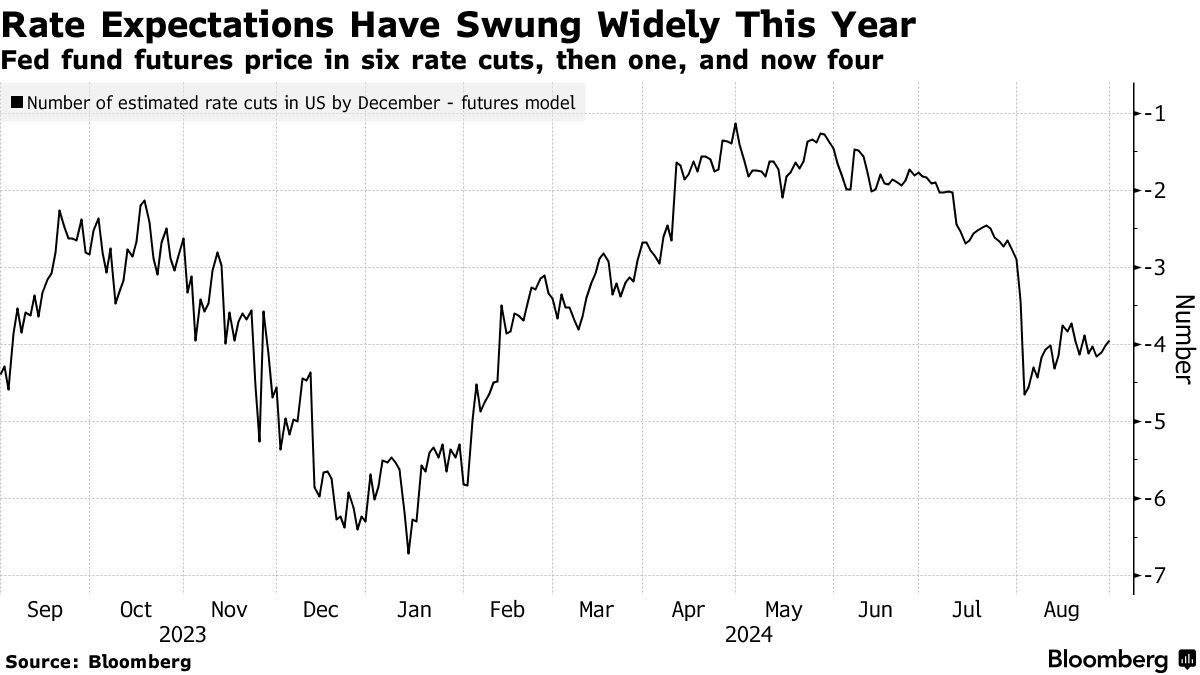

For a sense of the tenuousness, consider the path of rate cuts priced in Fed fund futures. Back in January, when inflation fears ebbed, bond traders wagered on roughly six rate reductions for all of 2024, with the first one arriving as early as March. When inflation proved stickier than forecast, those bets were pared and by April, only one cut was expected.

Now the consensus is, the Fed will kick off its easing cycle next month, with four quarter-point reductions by December.

“The reality is both the Fed’s own guess in the dot plot and the market’s expectations are always wrong,” said James St. Aubin, chief investment officer at Ocean Park Asset Management. “I could see easily three cuts this year. Four might sound pretty extreme. It would probably only happen if the economy was really in bad shape.”

At the same time, caution has mostly proved a costly investment philosophy this year. In the credit market, the much dreaded maturity wall — the threat of painful refinancings by corporate borrowers at higher rates — is collapsing as the amount of looming debt repayments in the junk bond market is poised for the biggest annual decline in at least a decade. Credit default swaps, or instruments designed to hedge exposure to credit risks, have retreated as the Markit CDX North American High Yield Index hovered near the lowest levels since early 2022.

Rather than taking a hit from higher borrowing costs as many had feared, corporate earnings may in fact have benefited from the jump in benchmark rates from 0% to over 5%. That allowed cash-rich firms, technology megacaps in particular, to enjoy a steady stream of income from their bond investments.

According to Kaixian Tan, an analyst at Gavekal Research, the entire increase in non-financial corporate income since 2022 can be attributed to a drop in interest payments on a net basis — a counterintuitive situation where booming interest income broadly offset rising debt service costs as rates rose. Now with interest rates heading lower, that tailwind is under threat.

“Rate cuts will squeeze corporates’ interest income, and therefore their profits,” Tan wrote in a note this week. “This will disproportionately hit big companies sitting on large cash mountains, and may lead to their relative underperformance.”

To Jack McIntyre, global bond portfolio manager at Brandywine Global Investment Management, predicting anything in the post-pandemic world is nearly futile. If he had to venture a guess, it’s that economic resilience will dull in the coming year and in that environment, bonds will beat stocks.

“To me, a soft landing is just a hard landing postponed,” he said. “I don’t think we go from soft landing back to a no landing.”

Written by: Lu Wang and Emily Graffeo @Bloomberg

The post “Once-In-Lifetime Wall Street Rally Raises Soft-Landing Stakes” first appeared on Bloomberg