- Dealers see long-term debt auctions held steady for now

- Focus of refunding guidance will be on coming quarters

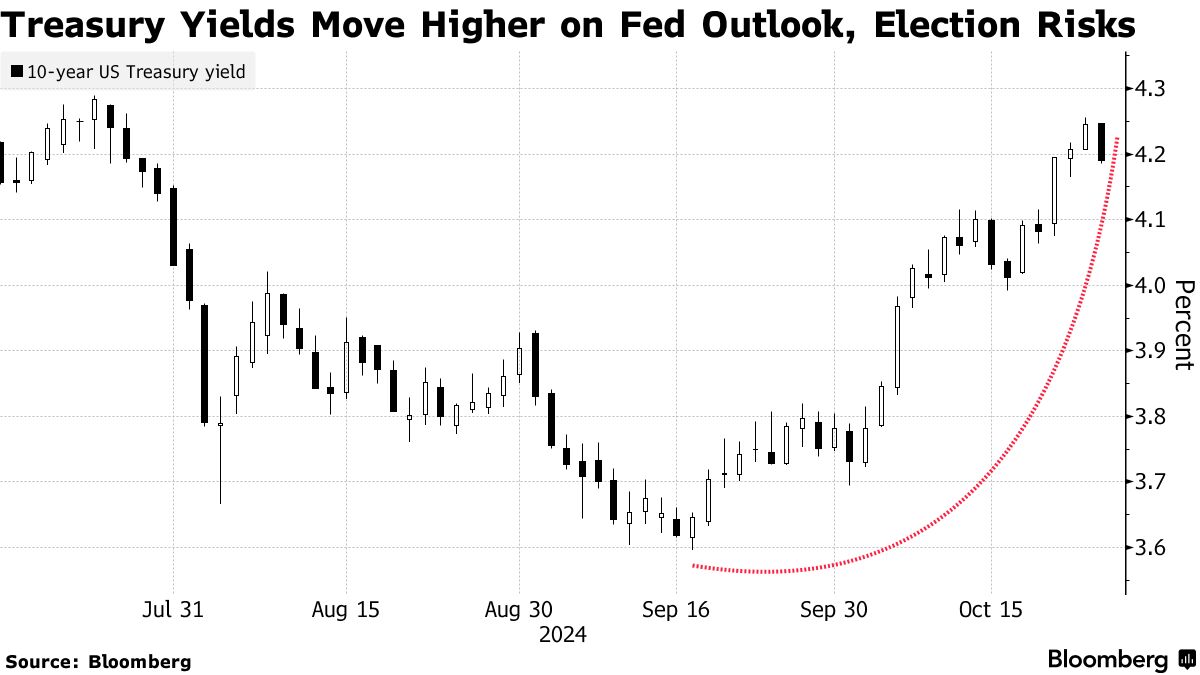

With its confidence in future interest-rate cuts shaken by US economic resilience, the Treasuries market is also facing doubts about how much longer the US government can avoid ramping up its borrowing.

Even as the US continues to clock historically large fiscal deficits, the Treasury Department since May has issued guidance that it will hold note and bond auction sizes as-is “for at least the next several quarters.” The next so-called quarterly refunding announcement is due Wednesday.

Bond dealers widely expect that the refunding auctions will total $125 billion for the third straight quarter. The question is whether the guidance about “several quarters” will be kept. If it remains, that would suggest avoiding any boost until no sooner than around mid-2025.

With neither former President Donald Trump nor Vice President Kamala Harris making deficit reduction a central element of their campaigns, the trajectory of US borrowing means that an increase in sizes of longer-term debt sales is seen as inevitable at some point.

“Saying ‘several quarters’ again seems like a pretty significant commitment for Treasury to repeat at this time,” said Thomas Simons, a senior economist at Jefferies. “But they may.”

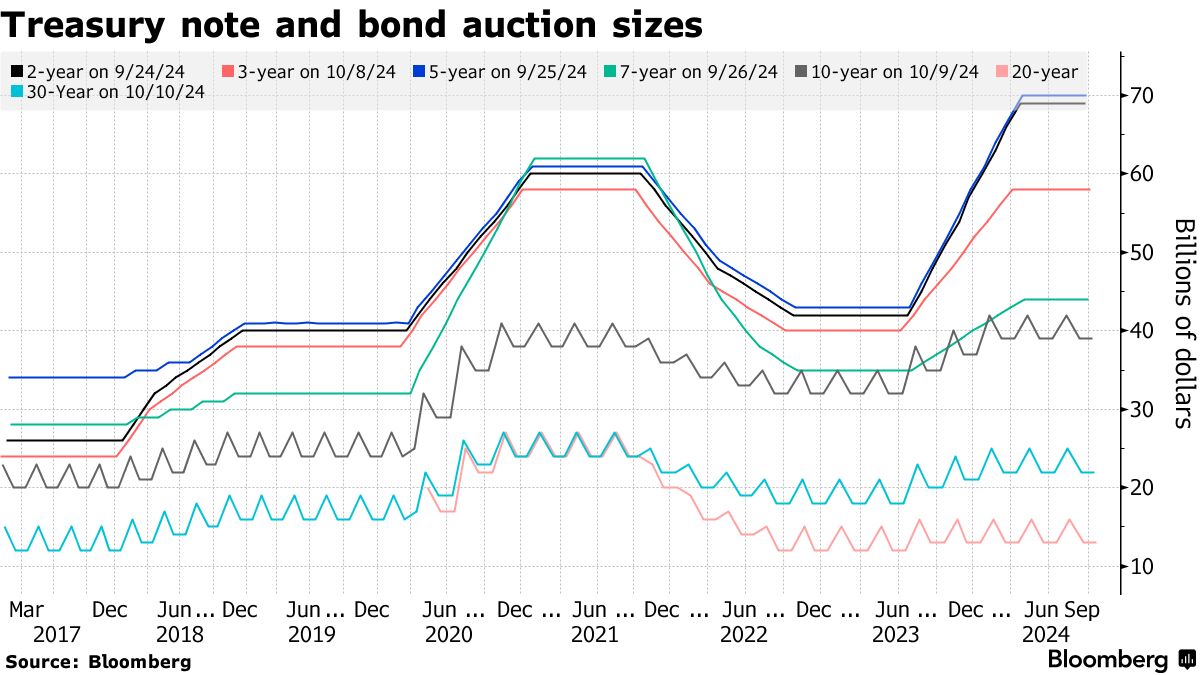

Some US debt auctions, including those for 10-year notes, have already reached record sizes. Any suggestion that increases are more imminent could further unsettle a bond market where yields have risen sharply over recent weeks. On Monday, traders will also get an update on the Treasury’s broader borrowing needs with the release of its quarterly financing estimates.

“This forward guidance is somewhat new from Treasury in terms of the refunding announcements,” Phoebe White, head of US inflation strategy at JPMorgan Chase & Co. “So it could spook the market if we do get a change in the guidance and see that language dropped.”

JPMorgan, along with firms including Citigroup Inc. and RBC Capital Markets, sees no changes on Wednesday to either quarterly sales or the forward guidance. Wells Fargo, for its part, expects a slight change in wording, but one that’s insufficient to roil investors.

“We think that Treasury is likely to tweak their guidance on coupon increases, but not in a way that would suggest that increases are imminent,” said Angelo Manolatos, a strategist at Wells Fargo.

But there’s a wild card this time. Wednesday marks the final refunding announcement for the Biden administration’s team.

New Team

The next plan is due after a new president takes office. And some Republican supporters of Trump have publicly blasted Treasury Secretary Janet Yellen and her lieutenants for boosting reliance on bills, which mature in up to a year, in order to keep a lid on sales of longer-dated securities, and their yields. That suggests sales of bills could be scaled back, and longer-dated issuance ramped up, if the GOP wins the White House.

Simons at Jefferies said it amounts to “a weird time — as far as how significant this guidance really is, given it’s just ahead of a presidential election. There’s a lot of things that key off the election results.”

Keeping the status quo for issuance sizes would put next week’s refunding auctions on course for the following:

- $58 billion of 3-year notes on Nov. 4

- $42 billion of 10-year notes on Nov. 5

- $25 billion of 30-year bonds on Nov. 6

What Bloomberg Intelligence Says..

“Treasury won’t need to alter its guidance as they may even be able to keep coupon-bearing debt sales stable for the next year. Given Treasury is already raising over $1.6 trillion in fiscal 2025 under current issuance, there’s little need for any adjustments unless there’s unexpected spending that needs funding.” ”

—— Ira F. Jersey, chief US interest-rate strategist

Even before any new team takes office, debt managers — who include career Treasury officials — will be contending with the resumption of the federal debt limit at the start of January. Unless Congress swiftly suspends or boosts the ceiling, the Treasury will need to kick off an oft-employed process of giving itself maximum space to keep making good on payments.

“If Treasury is under debt-limit constraints after January 1, they would not want to be lifting coupon supply,” said Blake Gwinn, head of US interest rate strategy at RBC Capital Markets. “So retaining the guidance of ‘several quarters’ more of stable auctions seems best.”

One dynamic expected in coming months that will help the department is a further slowdown of — or even an end to — the Federal Reserve’s quantitative tightening program. QT involves letting an amount of Treasuries mature off the central bank’s balance sheet without replacement, and forces the Treasury to sell more debt to the public.

Investors will also be looking for a fresh update from the Fed at the Nov. 6-7 policy gathering on the outlook for interest-rate cuts. Since the central bank kicked off its cycle of rate cuts with a 50 basis-point reduction last month, Treasury yields have climbed as investors reined in expectations for how low policymakers will bring down their benchmark in subsequent meetings.

The Treasury on Wednesday is predicted by dealers to keep issuance of floating-rate debt unchanged over the coming three months. With regard to Treasury Inflation Protected Securities, or TIPS, the department is seen continuing to edge some sales higher. In its quarterly survey of dealers, the department asked whether it should consider adding to its current lineup of three TIPS maturities.

Written by: Liz Capo McCormick — With assistance from Viktoria Dendrinou @Bloomberg

The post “Next Hurdle for Treasuries Is Whether US Keeps Debt Sales Stable” first appeared on Bloomberg