- UBS investment-bank research unit is underweight on stocks

- Country may suffer impact from Trump policies, China deflation

UBS Group AG is recommending to short India’s rupee and go underweight on the country’s stocks amid slowing economic growth, a trend that could worsen after Donald Trump takes over as US president.

The bank’s research group said India’s $4 trillion economy has entered a structural slowdown that can’t be explained by cyclical factors like oil-price hikes or declining government spending. The deceleration is underpinned by a long-term moderation in credit growth, foreign direct investment, export competitiveness and earnings potential, UBS said.

The “conventional wisdom that India is ‘far removed’ from Trump risk compared to other emerging markets is debatable,” said Manik Narain, head of EM strategy research at UBS. “A potentially higher-for-longer US yield environment poses challenges to India’s growth, with one of the highest debt service-to-revenue ratios in the major EM space.”

Indian stocks have lost almost $500 billion in market value in the past month, with MSCI Inc.’s index for the nation marking the worst start to a year since 2016. The rupee has fallen to successive record lows against the US dollar, the worst performance in Asia. The country’s bonds are recording the fastest outflows since 2020 as euphoria over their inclusion in global bond indexes wanes.

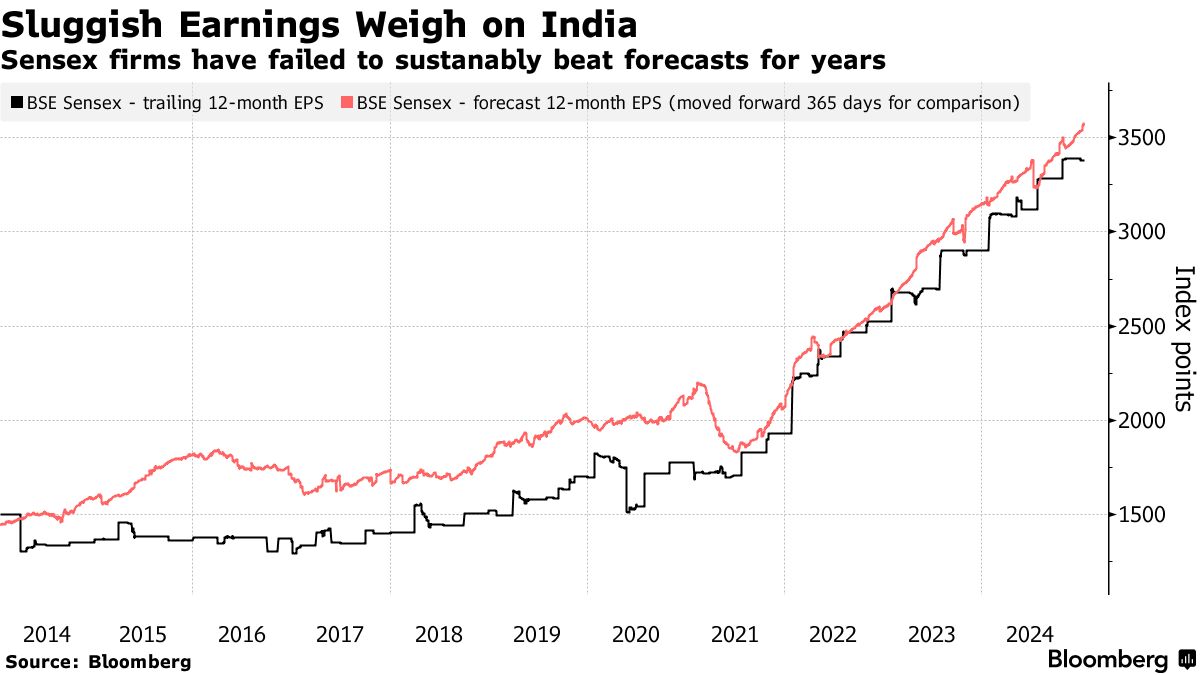

Market losses follow a slowing in real GDP growth over successive quarters, showing the Indian’s economy slipping below the 7% average generated before the Covid-19 pandemic. Disappointing business updates following a decade in which companies in the Sensex index failed to meet analyst expectations have underscored the bearish turn. Mounting external risks, especially from rising Treasury yields, are keeping policymakers from prioritizing growth.

Narain says the moderation in India’s earnings growth is spreading to defensive parts of the economy — such as the consumer-staples sector — showing that temporary factors such as government capital expenditure are not the only reasons behind the slowdown.

Other longer-term factors, according to UBS:

- Credit Moderation — The equilibrium growth rate in India’s credit markets will fall to about 10% a year compared with the average of 16% in the past two years, as the loan-to-deposit ratio — at 80% — is getting stretched to its highest on record, Narain said. That means future credit dynamics will increasingly depend on deposit growth if lenders want to avoid bad loans.

- China Deflation — A devaluation of the yuan in real terms and a drop in China’s export prices are challenging India’s industry by way of stiffer competition in overseas markets and cheaper imports, according to Narain. Data compiled by Bloomberg show that despite the recent selloff, the rupee trades more than two standard deviations stronger than its average, while the Chinese currency trades almost two standard deviations weaker than its own mean.

- Slowing FDI — While the country’s external account has raised investor worries, Narain said, a bigger concern for UBS is slowing FDI flows — to only $3 billion in the past 12 months — which is hinting at stalling equity investments.

- Market Participation — Calculations by UBS suggest that equity holdings represent 23% of the financial assets of Indian households and 60% of bank deposits. That means the market can no longer be termed “underpenetrated,” Narain said.

- Valuation — Based on the bank’s valuation methodology, the country’s stocks trade at a 72% premium to the rest of emerging markets, a premium “unheard of even 12 months ago.”

The Reserve Bank of India also faces a short-term dilemma around whether or not to cut interest rates. “The RBI is facing a tough balancing act, with high US rates meaning that monetary easing may erode rupee carry and hot money capital flows at a time when FDI and equity flows don’t quickly come in to compensate,” he said. “Yet, the economy needs stronger growth help.”

Narain said investors should buy bearish rupee options, pricing in a further 2.6% depreciation this year. However, the bank also recommends rate-receiver positions via five-year swaps to benefit from an eventual 75 basis-point rate reduction.

The rupee fell to 86.55 per dollar on Thursday. The currency’s one-year implied volatility, derived from options prices, rose and was on course for the biggest weekly increase since November.

Written by: Srinivasan Sivabalan @Bloomberg

The post “Short Rupee as India in Structural Slowdown, UBS Narain Says” first appeared on Bloomberg